Student Debt Crisis

Abigale Garpestad

Writing for Social Sciences/ ENG 21002/ City College of NY

May 14, 2019

Acknowledgements: Jose Reynoso, Annabelle Surya & Ayouba Kamara

Table of Contents

Abstract…………………………………………………………………….3

Introduction………………………………………………………………..3

Methods and Materials…………………………………………………….5

- Participants………………………………………………………..5

i. Field Observation Participants………………………………….5

ii. Interview Participants………………………………………….6

iii. Survey Participants……………………………………………7

b. Materials………………………………………………………….7

c. Procedure………………………………………………………….7

i. Field Observation……………………………………………….8

ii. Preliminary Research…………………………………………8

Iii. Survey………………………………………………………..9

Iv. Interviews…………………………………………………….10

d. Limitations……………………………………………………….11

4. Interviews Q&A……………………………………………………………12

5. Results

- Preliminary Research Results……………………………………………18

- Interview Results………………………………………………………..20

- Survey Results…………………………………………………………..21

6. Discussion………………………………………………………………….22

6. Works Cited……………………………………………………………….25

Abstract:

Students have been struggling to afford their higher education costs for decades, and those who can’t, are obligated to take out loans. These loans can accumulate to hundreds of thousands of dollars, making it difficult for graduates to create a life outside of debt. The purpose of the following study is to evaluate the remedies offered by financial aid/government officials to combat the student loan crisis. To gain an understanding of the severity of this crisis, interviews, and surveys were conducted with community representatives and individuals who have been negatively affected by their student loans. The survey results conclude that more than half of the students surveyed at Fordham University have taken out loans to cover tuition costs, whereas less than half of CUNY students surveyed have not taken out loans nor do they plan on taking out loans. It is no secret private universities are drastically more costly than CUNY schools. Nevertheless, attending a student’s top choice university should not bury them in a lifetime of debt.

Introduction

Achieving a higher education has become a necessity to high school graduates, as it appears to be the right path to lead a successful life. “Go to college, decide on a major, gain a diploma, and you’re set for life.” If only it were that simple. Completing a four-year degree doesn’t always guarantee you a career in the major you intended. You are instead guaranteed a hefty tuition bill. Whether you are completing your education at a public or private university, you may not be exempt from the debt that follows. The purpose of this study is to measure the severity of the student debt crisis and the remedies offered by the city and financial aid offices. The research has been gathered within a series of surveys and interviews with community representatives, college graduates, and current students. The questions proposed in the survey were intended to highlight the disadvantages student debt has presented to college graduates. Further background research was taken at A Neighborhood Trust Student Debt Crisis event. Real life scenarios were discussed along with personalized solutions.

The first student loans offered in the US transpired in 1840, available only to students attending Harvard University. Public loans have only become accessible as of the 20th century. During the 1940s, college attendance had increased drastically causing tuition to rise in accommodation. Gaining a higher education had become too expensive for families to pay for alone. The National Association of Student Financial Aid Administrators (NASFAA) was developed, with the sole purpose of helping students gain access to financial aid. Student borrowing became an option in the 1980s, which resulted in students racking up an alarming $10 billion in federal student loans- for the time being, this was an extreme amount to have in debt by US students as a whole. Today’s overall student loan debt is a whopping $1 trillion, plus.

The student debt crisis is consuming new students and college graduates alike. It is comparable to a recurring nightmare that you can’t quite escape soon enough. Not only does it affect how you live your life during your college years, but continues to linger in your plans for the future. College graduates may delay their desire for a family and home due to their outstanding debt. Home-ownership rates have decreased as a result of the irreparable damage. Parents of students currently enrolled must relinquish their freedom from debt to support their children upon signing a parent loan. Children of parents who have taken out private student loans may inherit their parent’s debt as well as their own. Many can attest that the system is flawed. It is a set up for failure.

The cost of student borrowing has increased immensely. Interest conducted on borrowing has risen to 5 percent just this year, totaling at 6.6 percent for graduate and professional degrees. Students on an interest-based payment plan witness their debt plummet before they have even completed their education. The long-term negative effects of the student debt crisis is a collapsing economy. The graduates seeking a reliable career to pay off their debt, enter the job field with a crippled credit score and must start from negative. When society as a whole is building a life with little stability, how can it ultimately flourish?

Methods

Participants

Field Observation Participants

The field observation was conducted at a Student Loans Workshop conducted by the Neighborhood Trust Financial Partners (NTFP) on Saturday, March 16th, 2019 in 2751 Grand Concourse, The Bronx, New York. Attending the workshop was a method in understanding/learning the statistics, problems, and remedies regarding those dealing with student debt. The speaker was Eric Espinoza, a financial counselor at the company who has dealt with many cases regarding student loans with his own clients. As a worker in the field and, thus, a very informed person on the subject, he agreed to set up an interview for the study over the phone.

One of the participants of the NTFP was Olga Baez, a woman who had a significant insight to share with her fellow audience members. She gave helpful tips based on her experience on how to save money during college and talked about how she had loans, herself. She was, thus, approached at the end of the meeting to set up an interview due to her potential in expanding upon her knowledge and insight regarding saving money and in student loans. She happily agreed. It was learned that Ms. Baez has started her own non-profit organization called Strive Higher NY, which helps young students of color reach out and explore different fields of study, guides them through the high school/college application process, and offers significant life advice.

Interview Participants

When researching the topic of student loan debt, priority was put on finding interviewees with experience in the topic. Potential interviewees consisted of school financial aid counselors, current students, and graduates/non-graduates with substantial loan debt. This would provide some helpful insight into what is being done to help students mitigate their student loan debt. Furthermore, speaking with an official who works in that area would provide extensive knowledge on how students or graduates should proceed with handling their debt. Lastly, interviewing a student or graduate with student loan debt would provide insight into how people affected by the crisis first-hand deal with their debt. Therefore, Eric Espinoza was interviewed for his experience as an advisor at Neighborhood Trust Financial Partners. Olga Baez was selected due to having the first-hand experience with student loans and having knowledge gained from initiating her non-profit organization, Strive Higher NY.

Survey Participants

Thirty successful, self-administered surveys were taken at the Lincoln Center campus of Fordham University in front of the main building. All participants were either currently pursuing a degree or have already graduated. Roughly ten people declined to take it.

Thirty more surveys were taken at the City College of New York. The surveys taken in the class were used, and the rest were taken from the online Google Form, shared on social media. Therefore, the CUNY group of students were either from the classroom or have a connection to a group member.

Materials

The materials used during the field observation was a notebook, a laptop, and the Student Loans Workbook that was provided. To conduct surveys, there were both physical copies and an identical Google Form that participants answered on. For the interviews, a cell-phone voice recorder was used, a cell-phone to talk was used, and laptops to take notes were used.

Procedure

Field Observation Procedure

A field observation was conducted on March 16, 2019, at a workshop hosted by the NYC Department of Consumer Affairs Office of Financial Empowerment, in cooperation with Neighborhood Trust Financial Partners, which sought to help attendants with their student loan debt and how to manage their repayment. It was in a large room similar to a classroom setting. Attendees sat at large tables facing the speaker who used a small whiteboard. The questions people asked and the tips they gave were paid close attention to during the workshop. It was hoped to achieve greater knowledge on the remedial measures of student debt provided by the government or other institutions. Using an informative, interactive guidebook, the workshop offered valuable insight on how to manage one’s student loan debt. It also provided a sense of the type of people who struggle with student loan debt. This field observation was participatory, but participation was kept to a minimum.

Preliminary Research

The first interview, conducted on Thursday, April 4th, 2019, was face-to-face in a semi-structured format in order to gather as much input as possible with follow up questions as the interview continued. The interviewee was Olga Baez, a former student of Fordham University who now works at the school and has founded her own organization which aims to help students get through college. A total of five questions were written prior to the meeting in order to guide the conversation and to ensure a touch on relevant points. The questions also aimed to collect as much insight as possible on Olga’s role in this field. However, many of her points were worth expanding upon, so a few additional questions were asked when appropriate. The second interview was conducted over the telephone on Tuesday, April 9th, 2019, for the interviewee’s convenience. This interviewee was Eric Espinoza, an associate director of programs and strategic advocacy for Neighborhood Trust Financial Partners. For him, questions were geared toward his specific experiences in working with people with student debt. His responses would thus lead to stories that magnify the severity of the issue, and he would offer his knowledge on student loan remedies. Similar to the prior interview, this interview was also semi-structured and consisted of four questions, which also aimed to gather insight on Eric’s role. This semi-structured method allowed Eric to follow-up on his responses to clarify certain points or to expand on his responses. Furthermore, both interviews were recorded on a telephone recorder and notes were taken as the interview took place.

Survey Procedure

Surveys were conducted in order to collect data on the number of student loans taken out by college students, as well as how those students would deal with the debt. The target audience included graduates or current college students as they were more likely to offer insight on their experience or expected experience with student loans. The focus was put on surveying students of Fordham University and students of City College. Fordham University was chosen due to the school’s reputation for high tuition. Because of this, students of Fordham University were more likely to be on the severe end of student debt and were be able to provide significant responses regarding their experiences. City College was chosen because it is a CUNY school, therefore providing insight on the issue of student debt from another perspective.

A total of eight questions were asked on the survey. The surveys administered were intercept surveys. The questions on the survey mainly consisted of multiple choice questions, with one dichotomous question and one open-ended question. The variety in question types allowed for the categorization of these responses in order to compare results. The demographic questions related to income, level of education, and occupation. To allow the surveyed to be more comfortable sharing income level, ranges were provided for each answer. The other questions focused on their experience with student loans, whether they have it or not, so anyone may provide feedback about how they feel towards student loans. To create a space for this feedback, the open-ended questions asked if the degree was worth the debt, and what can be done to help remedy the crisis.

The physical survey was conducted on April 4th, 2019 between the hours of 1 pm to 3 pm. Participants most important to this study were those with some amount of student loan debt, therefore, students at the Fordham University Lincoln Center Campus, located at 113 W 60th Street, New York, NY, were targeted. Of the participants approached, 30 responded. Surveys were also conducted online via Google Forms from April 4th, 2019 to May 8th, 2019. Furthermore, surveys that were conducted on physical paper at Fordham University were transferred to the Google Form. This format was chosen because of the ability to obtain a higher reach than stay within the limits of paper copies, time constraints, and physical boundaries. A Google Form was being sent to an audience that was unable to be reached otherwise. Also, a Google Form automatically categorizes results and creates a visual of the responses, which was convenient when creating charts and graphs in Microsoft Excel.

Interview Procedure

Potential interviewees were selected based on their knowledge and/or experiences with the student loan debt crisis. The target interviewees comprised of: one who is knowledgeable of the issue and works closely with student debt remedies, one who experienced student debt his/herself and can provide his/her story, and one who works in a financial aid office at Fordham University to discuss his/her advisement to students regarding loans. A total of five interviews were requested. Of the five interviewees, two responded. Interviews were conducted on April 4th, 2019, and April 9th, 2019.

Limitations

The most prominent limitation of the study is the survey’s respondents; feedback from students and graduates was crucial, thus surveyees were chosen based on a convenience sample of the students who were around Fordham’s campus at a specific time, meaning their responses could not be generalized to the entire school. This also highlights another limitation that was present in the study: sample size. In order to get more accurate data, a larger sample size of more than 1,000 would be needed. This is due to how big of a situation the student loan debt crisis is and the fact that it affects many students in the country as a whole. This kind of sample size would prove to be impossible, however, given the time constraints on the study.

Furthermore, the study would have benefitted from responses of various other groups. Input from government workers would have been very valuable. A worker in Department of Consumer Affairs should have been contacted for their input in what New York can expect in the future in terms of student debt, and what is currently being done to remedy the crisis. The study would have also greatly benefitted from surveying students who attended other private, non-profit colleges. In this study, only one private college was looked at. In order to gather more insight and better data, more colleges could have been involved in the study. However, due to time constraints, it proved to be difficult to involve other schools aside from the two already involved.

Field Observation Results

By attending the workshop, many attendees were older and most of them had already completed college and were currently in debt. One man, who spoke a lot, had just finished paying off his loans and seemed to be there just to offer advice or gain knowledge to share with other people. There were several remedial measures to student debt offered, and the most significant was simply awareness on the options people have regarding paying off their debt, and options besides debt, such as scholarships and government aid. A way to best understand these options is taking advantage of the free financial advisement given by one of New York’s Financial Empowerment Centers. Many people inquired about loan forgiveness, and it was learned that loan forgiveness is difficult to achieve.

Interview with Eric Espinosa

An interview with Eric Espinoza, a financial advisor at Neighborhood Trust Financial Partner, was conducted on March 16th, 2019. The interview took place over the telephone and lasted close to 27 minutes. Various questions were asked about his field of expertise and personal opinion on the matter. Three group members were present; one member asked the questions, one member recorded the interview, and one member took notes as the interview continued. The interview began with introductions between the three group members and Eric Espinoza.

Jose: What work have you done specifically to assist students struggling to pay their student loans?

Espinoza: I started as a financial counselor in Neighborhood Trust in 2012 and a lot of work is divided into categories. There were those who their employers gave them everything that was promised and they were able to get a job in an area where they could manage all the goals they had in order to focus paying back student loans and help them prioritize their student loans payment goal and help their family members, that was one category how would directly help people to back their student loans.

The other thing is to make them aware the payment program that they have access to, would allow them the most flexibility and fit in other priority that they have as a potential student loans forgiveness program that they had explored. Those are kind of the happier side of student loans programs, but the frightening side is how to get their loans out of default. That’s what would happen to your student loans if you are unable to pay them back within nine months.

You know a number of things we will do are to negotiate with federal to try a lower student loans payment temporarily or permanently based on the way they were trying to get back on track.

Jose: How do you feel the government can improve the student debt crisis?

Espinoza: There are a lot of things they can do. I think that there is generally a lack of awareness, first of all, they can make signing up for student loans a lot better, more comprehensive and more understandable also give true information for both student borrowers and their family members. They should tell them what kind of loans they qualify for in order for them to be able to pay them faster; because some schools do not clarify what students need in order to borrow just for their tuition, but generally the living cost and books are all stuff that student must have for their education that what makes it a little harder. And they need to make the repayment plans simpler. There needs to be a plan for students to ensure their senior year, then when they graduate, they will know what to do to pay off their debts. Also, the local government could really help on where students could go for free advice because, with this crisis, a lot of people are getting rich just to help people learn how to manage their student debts.

Jose: In your personal opinion, do you think a college degree is necessary to lead a successful life?

Espinoza: You know I feel like that a tricky question. No, but It depends on how you define success, some people want to live life with relatively low stress and meet people all around the world or being a parent. I think there are a lot of ways to be successful without a college degree, but realistically in the job market that exists right now, it’s very difficult to access a stable full-time job without a college degree. I think the concern should be what you pay for a college degree and how much of the quality degree you got. Do employers care how much you pay to earn that degree? Those are the concerns.

Jose: What is the worst situation you have witnessed as a direct result of student debt?

Espinoza: There are so many, I think one example is there was a student who got behind on his student loan payments and was trying to resolve by buying them back. The department of education hired some people to try to help those who are back in their repayment. A certain amount is paid to that collection agency. So the late borrowers have to pay another amount just to get back on track. Sometimes they also are planning to take people’s social security payment but they are supposed to do that. I think that those are the worst situations I have witnessed.

Conclusion: This interview was full of information and enthusiasm from our group and Eric Espinoza. we were appreciative of his thoughtful and informative responses.

Interview with Olga Baez

Annabelle: Tell me about Strive Higher NY and your role in it.

Ms Ortiz: Sure, so I started Strive Higher NY in summer 2017, the idea is to expose middle school students of color and high school students to different experiences and opportunities, so I take them on college fairs and we focus on literacy and career. The idea is to get students prepared for the future and start thinking about all differences and opportunities out there and teaching them financial literacy and different careers that are available. We help them to get scholarships and internships with some financial institutions…(she smiled) it is a one woman show, I run the program by myself. I also help students know how to graduate from college, because what’s the point of going to college if you don’t graduate from it.

Jose: What is your experience regarding student debt? What brought you the Student Loans Workshop? (If you did take out loans, how did you go about paying it back?)

Ms Ortiz: I wanted to figure out what they were offering, that was the reason that I went there, because I don’t see many events in the bronx like this and it seems to be working together, so I wanted to see and I was very happy that they got so many details and informations to share and I wanted to also share that information with others. When it comes to my personal experience, I am a first generation college student, so I went to college I knew that I didn’t want to get in debt. I didn’t say that “oh I am going to go to a college that I want and take my student loan,” I took out a loan in my second year, but I was able to decrease it because of my job position. It was an HRS position. I was able to graduate without a huge amount of student loan, then when I went to grad course, I knew that I am going to have to spend a little bit more. What I can tell people is that if you really want to have a higher education, you need to be careful with the amount a debt you are taking while you still as undergraduate, because you are going to take out a loan if you want to pursue your master or Phd. Some students even get paid cut fee base on their status, so it’s better to know about all these opportunities that my lighten your loan.

Jose: Do you mind sharing how much student loan that you took out?

Ms Ortiz: Yeah sure it’s fine, you know working here as a Sophomore undergraduate, I will say it’s definitely under $20,000, and I graduated in 2005, so a long time ago, it was a small college but I did get accepted into PES, and the financial package was completely different from a small school so I was scared to go PES. You know when you graduate from college they give you 6 months, then after you’re gonna need to pay your student loans. So right now I would say that I have about $45,000 as student loans with interest with my college degree. I got two master degrees so I would say that it’s a lot money but it’s worth what I have received from it. I am on a 10 years plan with the process that I am on right now, I think I am going to be able to finish pay off in 10 years.

Jose: What would you advise new students (debt free) to do to remain debt free?

Ms Ortiz: I think they should continue to apply for scholarships. and continue to save up their money if you are working, with these methods, It will be definitely hard to be in debt.

Jose: What made you realize you were going to get involved? (personal connection to the topic?)

Ms Ortiz: Sure, I think my experience growing up as first generation college student has definitely paved the way and made me the person I am today. Unfortunately I don’t think that a lot things have changed since my time in high school and that’s sad. I think that there are a lot of programs but not as much for students to get their degrees. The numbers keep going up for students enrolling in college but not the same as they graduate. It’s great that blacks and latinos are going to college, but on the other side, how many of them graduate from it. Statistics show that 36% of students graduate from 2 years college within 3 years.

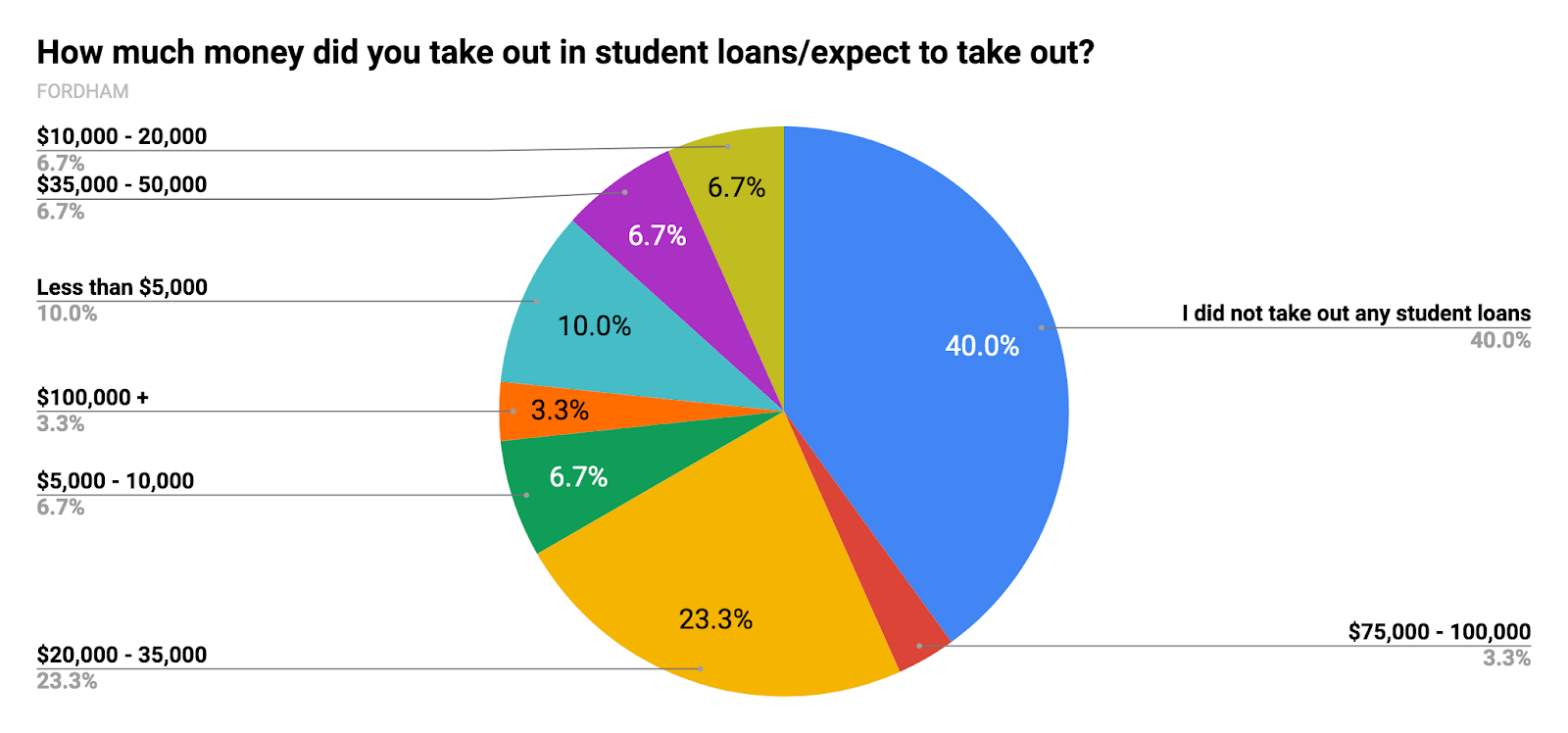

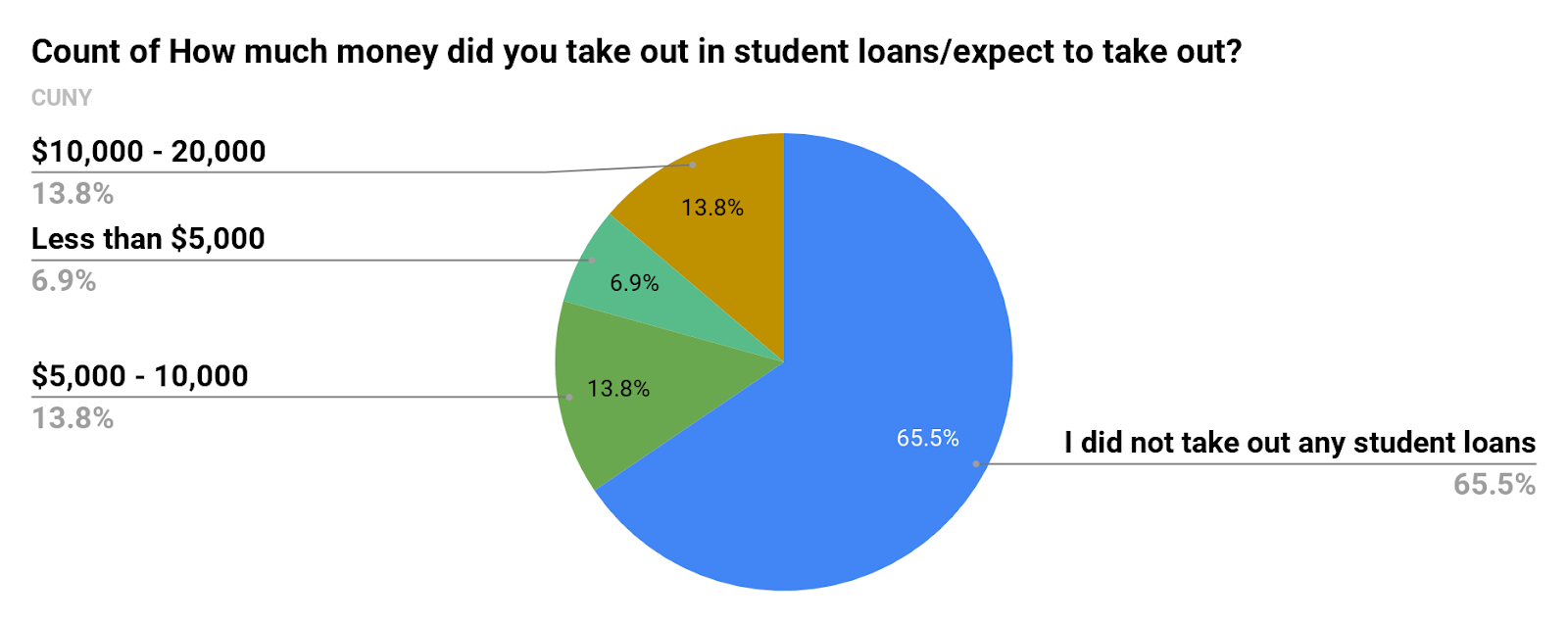

On a survey conducted at Fordham University and CCNY, we compared student loan rates taken out at both schools. Fordham University is a private university, while CCNY is a CUNY school.

Survey Charts:

FORDHAM:

This is the results found from the 30 people who were surveyed at Fordham University.

CUNY:

These are the results found from the 30 people surveyed at CCNY

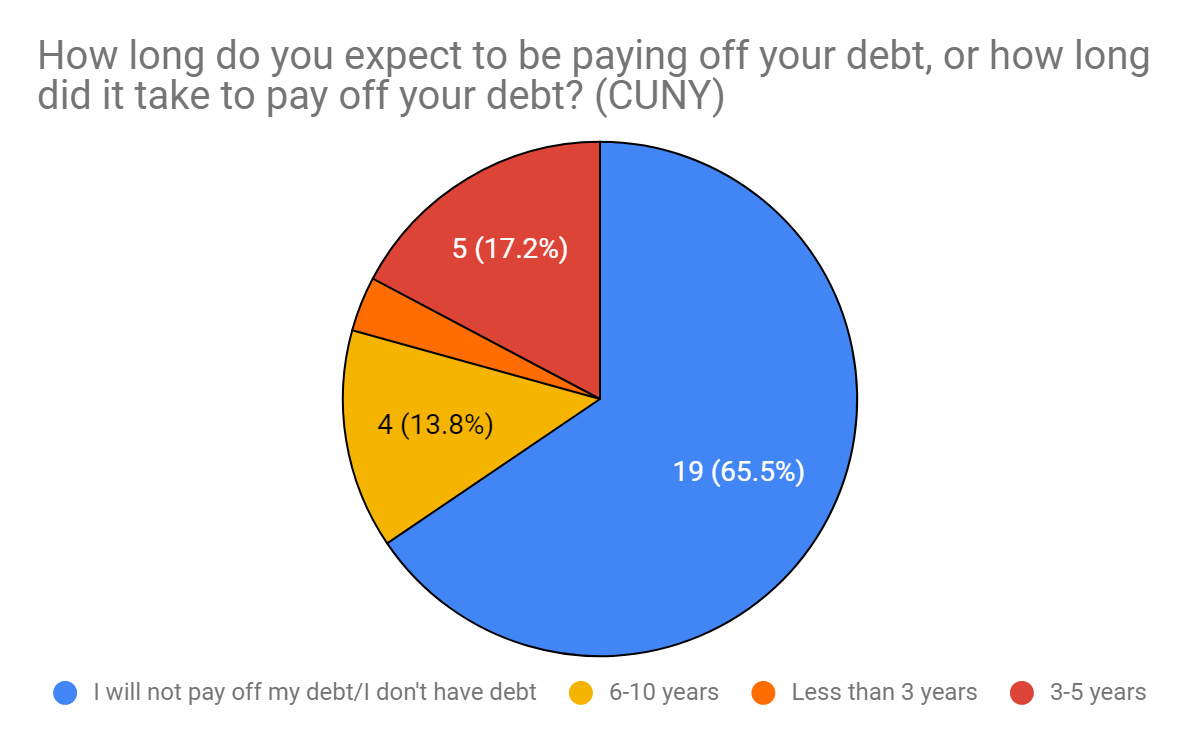

We then compared the length of time CUNY students and Fordham University students expect to be paying off their loans. Considering the tuition at Fordham University exceeds CUNY tuition, Fordham students intend on taking out more loans which will in turn take longer to pay off.

Interview Results

We interviewed two experts in their domains and the interviews were conducted in different manners. The first interviewed happened at Fordham University, it was 40 minutes long and the interviewer name was Olga Ortiz, She is the founder of Strive Higher New York in summer 2017, during the interview, Ms. Ortiz explained to us why she created this initiative. As a resident of the Bronx, She wanted to help those who cannot get access to a certain type of education, especially Blacks and Latino. She also aids middle school and high school students in preparing for college life. She helps them apply for scholarships, get well informed about student loans and also apply for internships. She is a borrower herself and currently owes 45,000 dollars in student debt, but she doesn’t regret her decision to take out loans because it has helped her earn two master degrees.

The second interviewer works for Neighborhood Trust Financial Partner, his name is Eric Espinoza. The interview with Mr. Espinoza was conducted via phone call and lasted more than 25 minutes long. During the interview, Mr. Espinoza explained his role as a counselor in Neighborhood Trust, including the function of this organization to assist in the student debt crisis and what role the federal government can play to improve this situation.

Survey Results:

As expected, students attending Fordham University have taken out significantly higher amounts in student loans than CUNY students, and expect to take double the amount of time to pay them off. 23.3% of Fordham University students surveyed have taken out $20,000- 35,000 in student loans. 3.3% said they have taken out $75,000-100,000 in loans and another 3.3% have taken out over $100,000 to cover tuition costs. Meanwhile, students surveyed attending CUNY have taken out no more than $20,000 in loans. Students attending CUNY schools have a greater chance of not having taken out loans than private university students.

A whopping 65% of students surveyed who attend CUNY have not taken out loans. A drastic difference from the 40% of Fordham University students surveyed who have not taken out loans. The other 46.7% of students attending Fordham University believe it will take no more than 5-10 years to pay off their loans. And 3.3% believe it will take over 26 years to pay off their student loans, comparative to CUNY students who believe their loans will be paid back within a maximum of 6-10 years. Even so, a majority of CUNY students who have taken out loans believe it will take 3-5 years to complete.

Discussion

The purpose of this study was to evaluate the severity of the student debt crisis and the remedies being offered by financial aid officials. Prior to developing research on this topic, I was prepared to be overwhelmed with stories of college graduates in unsalvageable debt. Instantly it was clear I had made a correct assumption. Student loans are designed to be appealing to college students. It is advertised as free money that you will have the luxury of paying off once you are established. It is a common misunderstanding that students will have to begin making payments six months after graduation to avoid interest on their loans.

Students are too eager to take out loans and aren’t properly educated on the consequences of unpaid loans. Unfortunately, financial aid guidance is flawed in that department. Financial aid officials should provide a thorough break down of the different payment plans graduates can choose to fit their needs. When borrowers choose a plan that is unrealistic, it is often inconvenient and unaffordable for their current situation. Most times, they are unaware of the alternative plans.

As far as results go, we were correct to assume the student debt crisis is not a top priority to government officials. The financial aid system appears to be underdeveloped as many viable options are not being promoted, but rather a standard payment plan is set in place. This universal plan is what students are expected to be able to afford. As the student debt piles up, it is clear that is not the case. Since student debt is such a hot topic at the moment, we were anticipating a larger majority of our surveyees to have experience with loans. We were pleasantly surprised by our results.

Upon attending the Student Loan event, it was evident the attendees were educated and showed a great deal of investment towards the cause. People of all ages and race attended the event held in the Bronx early on a Saturday morning. Questions arose from financial aid officials attending the event as well as, burrowers (past, current, etc.), and parents fearing their child’s entry into student loans. The goal of the event was to start open conversation about the concern and offer guidance to those in need. The Neighborhood Trust Financial Partners representatives met and exceeded expectations as this was the first event of its kind.

We conducted surveys to gain an accurate gauge of the severe financial situations student loans has placed on burrowers. 27.6% of CUNY students surveyed say they have taken out anywhere from $5,000-20,000 in student loans; $20,000 being the largest amount surveyed to have been taken out. 43.3% of students attending a private university say they have taken out between $5,000-100,000+ in student loans. To gain perspective, the average salary of a full-time minimum wage employee is around $50-60k annually. The student loan payment plan involves monthly payments, separated from any existing expenses such as, rent, groceries, electric, transportation, etc. This is often a burden and an unrealistic standard for someone making this annual income. In New York today, the average salary is $69k. The numbers simply don’t add up. How can a minimum wage employee or a person of unemployment afford to make such payments when they exceed their limitations?

Considering the mass concern surrounding the future of student debt, our interview questions were geared towards gaining tips and useful information to avoid falling into the trap. Our interviewees felt it was of great importance this information be shared. Burrowers should know the risk in which they are engaging in and how to prevent further damage. It would be interesting to dive deeper into the behind the scenes of the student loan ideology. The purpose for the unclear spread of information about loans. It is a major issue and will go on to hurt future generation. How is the government benefiting from this and have they considered the consequences?

Works Cited

Dmarkski, S (2016, July 9) America Can Fix it’s Student Loan Crisis. Just Ask Australia, The New York Times, retrieved from http://www.nytimes.com

The purpose of this article is to discuss the differences between America’s student loan program compared to Australia’s. Australia has created methods to repair student’s debt and prevent further destruction of the economy as a result of the student debt crisis. The repayment system in America is flawed and in the need of improvements. It hasn’t changed since the cost of higher education has increased. There must be adjustments to make it possible for students to graduate without unworkable

debt. In Australia, students are only expected to begin to pay back their loans once they have an annual income of 40k.

Chinni, D, and Bronston S (2019, March 17) The Real College Crisis: Student Debt Drags Down Economy, NBC News, retrieved from https://www.nbcnews.com/politics/meet-the-press/real-college-crisis-student-debt-drags-down-economy-n984131

Studies presented in this article confirm that more millennials is in debt as a consequence of taking out student loans rather than credit card or mortgage debt. Homeownership has decreased by 4 percent in each age group. This article suggests that investing in higher education can be beneficial for the future of millennials, but considering the unhealthy damage that trails behind (financial instability and debt, etc), it is creating a crumbling economy for the next generations. Millennials

ages 18-34 have a positive view of the term “socialism” whereas anyone over the age of 34 felt a negative tie to the term. Younger voters tend to lean on the liberal side of politics, and some left candidates have a more positive association with the term. After obtaining an education in hopes of leading a successful life and achieve the American dream, students are drowning in debt and must postpone their plans. Because of this, millennials have a distorted view of the economic system; they are

more open to change in the system

Friedman, Z (2018, November 28) Betsy DeVos: Student Loan Debt Is Now A ‘Crisis’, Forbes, retrieved from https://www.forbes.com/sites/zackfriedman/2018/11/28/student-loan-debt-crisis/#67455cae21e3

“According to DeVos, student loan debt has tripled since 2007 and has risen by $500 billion since 2013.” DeVos provides several solutions to combat this crisis, including, implementing more conscious decisions when considering borrowing student loans. She suggests making student loan repayment plans simplified instead of the complex options currently available. The article offers ways to manage your student loan debt, such as paying off your student loans faster, enrolling in student loan forgiveness,

and to refinance student loans.

These articles provided me with an accurate depiction of the severity of the student debt crisis, enabling me to incorporate statistics and the remedial measures available.

Appendix

| II. Student Demographics | Bachelor of Architecture | 42 | ||||

| Age | Undergraduates | Masters | PhDs | Total | Bachelor of Arts | 1270 |

| 19 | 1805 | 0 | 0 | 1805 | Bachelor of Engineering | 369 |

| 20 – 22 | 4837 | 120 | 0 | 4957 | Bachelor of Science in Education | 76 |

| 23 – 24 | 1596 | 364 | 2 | 1962 | Bachelor of Science | 603 |

| 25 – 29 | 1718 | 950 | 35 | 2703 | Bachelor of Fine Arts | 63 |

| 30 – 44 | 1062 | 824 | 40 | 1926 | Master of Architecture | 20 |

| 45 & OVER | 287 | 272 | 3 | 562 | Master of Arts | 143 |

| UNDER 19 | 2601 | 0 | 0 | 2601 | Master of Science in Education | 162 |

| Total | 13906 | 2530 | 80 | 16516 | Master of Engineering | 68 |

| Gender | Master of Fine Arts | 46 | ||||

| Women | 7232 | 1515 | 26 | 8397 | Master International Affairs | 23 |

| Men | 6674 | 1015 | 54 | 7617 | Master Philosophy | 25 |

| Total Gender | 13906 | 2530 | 80 | 16516 | Master of Professional Studies | 26 |

| Ethnicity | Undergraduates | Masters | PhDs | Total | Master of Landscape Architecture | 14 |

| Asian | 3314 | 309 | 9 | 3632 | Master of Public Administration | 11 |

| Black | 2143 | 420 | 5 | 2568 | Master of Science | 141 |

| Hispanic | 5364 | 697 | 7 | 6068 | Master of Urban Planning | 8 |

| American Indian or Alaskan Native | 21 | 2 | 0 | 23 | PhDs | 30 |

| Non-resident Alien | 848 | 276 | 41 | 1165 | Total Degrees Conferred | 3147 |

| White | 1957 | 799 | 18 | 2774 | V. Retention and Graduation | |

| Two or more races | 226 | 26 | 0 | 252 | (First-time, Full-time Freshmen) | |

| Native Hawaiian or Other Pacific Islander | 33 | 1 | 0 | 34 | 2011 Cohort six-year graduation rate (%) | 49.6 |

| Total Ethnicity | 13906 | 2530 | 80 | 16516 | 2017 Cohort one-year retention rate (%) |